%20(1500%20x%20800%20px)_2024.jpg)

What Does the One Big Beautiful Bill Act Mean for You?

On July 4th, President Trump signed into law what is commonly called the One Big Beautiful Bill Act (OBBBA). Several tax law changes set to expire at the end of 2025 were made permanent. Other tax law changes ended certain other deductions and credits. The combination of new or expanded income exclusions, deductions, and credits, along with other credits and deductions that were eliminated may lead to different tax outcomes for individuals, depending on their specific situation.

Our team at Elwood & Goetz has compiled and summarized a short list of changes that we believe apply to many of our clients. However, changes to the tax law were extensive, and depending on your situation, other provisions not discussed below may be impacted. If you would like to discuss how the OBBB could affect your tax situation, please let us know. Our team of financial advisors and tax specialists are here to help!

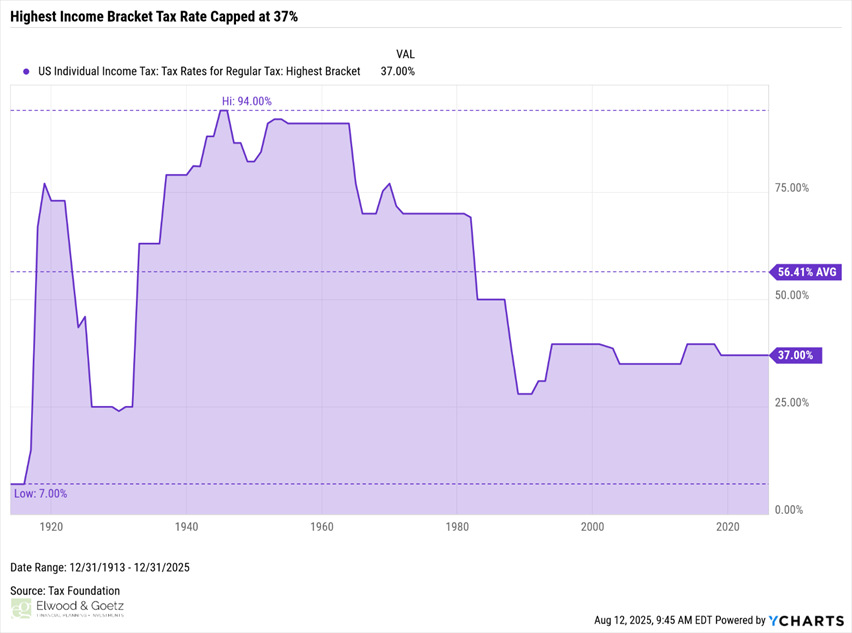

Historically Low Tax Brackets

OBBB retains the marginal tax brackets that are currently in place, avoiding what was set to be an increase in tax rates across the board. The top rate of 37% (for incomes above $750,000) is still below the historical average.

Enhanced Deductions

Standard Deduction. Permanent: Increases base standard deduction and inflation adjustments for all tax filers.

- Beginning this year (tax years starting after Dec. 31, 2024), the standard deduction will increase to $15,750 for single filers and $31,500 for joint filers. Future Chained-CPI inflation adjustments will use 2024 as the base year.

- Congress permanently eliminated the personal exemption deduction, which the 2017 Tax Cuts and Jobs Act suspended from 2018 to 2025.

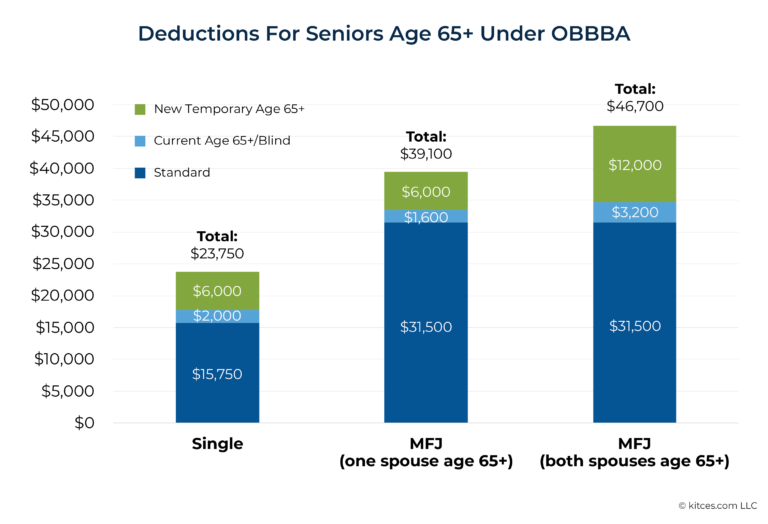

Senior Deduction. Temporary: The OBBB introduced an additional deduction for taxpayers 65 and older. This deduction is available for tax years 2025 - 2028.

- An additional $6,000 deduction is available for each individual who is age 65 and older.

- This deduction begins to phase out for individuals with an adjusted gross income (AGI) greater than $75,000 (S/HOH) and married filing jointly taxpayers with AGI above $150,000 (MFJ).

- The phase-out is 6% of AGI, which exceeds the phase-out limit.

- This deduction will not lower AGI, and is taken as a deduction from AGI when calculating taxable income.

Considering all these changes, a married couple with an Adjusted Gross Income (AGI) less than $150,000 who are 65+ will see a 44.5% increase in their standard deductions compared to 2024!

*Note: Congress did not change the taxation of Social Security benefits. The new Temporary Senior Deduction offsets taxable income for taxpayers who have not phased out of the deduction. This general deduction is not limited to Social Security benefits or any specific type of income.

Brand New Deductions

No Tax on Tips. Temporary: The OBBB created a new temporary ‘No Tax on Tips’ deduction for those who work in fields where tipping is customary (i.e., food and beverage industry). The deduction is available for tax years 2025 - 2028.

- Eligible taxpayers can deduct up to $25,000 in qualified tip income reported by their employer.

- Congress introduced additional reporting requirements to track tip income and the associated deduction.

- This deduction begins to phase out for individuals with an AGI above $150,000 (S/HOH) and $300,000 (MFJ).

- The deduction is reduced by $100 for every $1,000 AGI that exceeds the phase-out threshold.

- This deduction will not lower AGI, and is taken as a deduction from AGI when calculating taxable income.

No Tax on Overtime. Temporary: The OBBB introduced a new temporary deduction for overtime pay. The No Tax on Overtime deduction is available for tax years 2025 - 2028. Only those eligible to receive overtime pay under the Fair Labor Standards Act can claim the deduction for overtime pay.

- Single taxpayers can deduct up to $12,500 ($25,000/MFJ) of eligible overtime income reported on their W-2.

- Additional reporting requirements have been introduced to track eligible overtime pay.

- Similar to the tip income deduction, the overtime pay deduction begins to phase out for single taxpayers with AGI above $150,000 (S/HOH), and $300,000 for taxpayers filing married filing jointly.

- The deduction is reduced by $100 for every $1,000 of AGI that exceeds the phase-out threshold.

- This deduction is taken after AGI has been calculated and will not lower AGI. It is available to those who claim the standard deduction.

No Tax on Car Loan Interest. Temporary: Up to $10,000 of auto-loan interest is deductible when a loan used to purchase a new qualifying vehicle is taken out (or refinanced) after December 31, 2024. The deduction is available for tax years 2025 - 2028.

- Deduction begins to phase out for individuals with an AGI over $100,000 (S/HOH) and $200,000 (MFJ).

- The allowed interest deduction is reduced by $200 for every $1,000 of AGI that exceeds the phase-out threshold.

- The vehicle subject to the loan must meet the following requirements:

- Final assembly must be completed in the U.S.

- The vehicle’s original use commences with the taxpayer.

- Cars, minivans, vans, trucks, SUVs, and motorcycles are all eligible.

- Taxpayers can rely on the vehicle’s place of manufacture as reported in the vehicle identification number (VIN) to determine the location of final assembly. The IRS encourages taxpayers to use the VIN decoder website to determine if a vehicle was manufactured in the U.S.

- The VIN must be included on the tax return.

- This deduction is taken after AGI has been calculated and will not lower AGI. It is available to those who claim the standard deduction.

*Note: To take advantage of the full $10,000 interest deduction, a household must carry approximately $200,000 in auto loan debt on eligible vehicles, assuming a 5% interest rate, and be below the AGI phase-out thresholds.

State and Local Tax (SALT) Cap Increase. Temporary: For tax years 2025 - 2029, the OBBB increases the cap on State and Local Tax itemized deductions.

- For 2025, the limit has been increased for state and local tax itemized deductions from $10,000 to $20,000 for single taxpayers (S/HOH) and $40,000 for MFJ.

- The increased cap for state and local tax itemized deductions phases out when AGI exceeds $500,000.

- The cap is reduced by 30% of the amount of AGI in excess of the phase-out threshold. Taxpayers with AGI over $600,000 will be completely phased out of the higher cap.

- The cap will not be reduced below $10,000 for taxpayers in the phase-out range.

- Both the cap and phase-out threshold increase by 1% per year for tax years 2026 - 2029.

- Pass-Through Entity Taxes (PTETs) are still allowed for small business owners who pay state taxes through their business entity.

Education Planning. Permanent beginning in 2025. OBBB expands the flexibility of 529 plans for K-12 education. Up to $20,000 can now be withdrawn tax-free from a 529 for eligible expenses. In addition to tuition, the list includes:

- Public, private, or homeschool expenses.

- Tutoring costs.

- Curriculum, books, instructional materials, including online resources.

- Standardized testing.

- Dual enrollment.

- Physical, occupational, behavioral, speech-language, and other therapies for students with disabilities.

In addition, expenses used towards obtaining or maintaining a postsecondary credential are now considered qualified expenses for 529s. The credential must be “industry recognized” or accredited by a major credentialing organization or recognized by the U.S. government. Eligible expenses include:

- Exam fees.

- Tuition, books, and other requirements for enrolling in the credentialing program.

- Continuing education.

Clean Energy Credits Expiring. Terminating in 2025.

- Electric Vehicle Tax Credits (up to $7,500) are set to end on September 30th, 2025. Those seeking to claim this credit must acquire a qualifying electric vehicle before September 30, 2025.

- Residential clean energy and energy-efficient credits will expire on December 31, 2025. Residential energy-efficient projects must be completed and placed in service by the end of the year.

“Trump Account,” New Tax-Deferred Investment Account. Permanent. Beginning in the summer of 2026, taxpayers can make non-deductible contributions of up to $5,000/year to an account for eligible minors called “Trump Accounts.” The accounts generally follow IRA rules, but there are some distinct differences.

- Contributions are capped at $5,000 and can be made by many different parties, including employers, family, and charitable organizations. Employers have a cap of $2,500. Contributions from philanthropic organizations are not capped, but other requirements are imposed on the charitable organization.

- The contributions are after-tax and will create a tax basis in the accounts, requiring the keeping of good records.

- Temporary Government Seed Money. For U.S. citizens born between January 1, 2025, and December 31, 2028, the federal government will contribute $1,000 to their account. This contribution is deemed to be earnings when distributing the money.

- Investment options are limited to index funds with expense ratios less than 0.1% that invest in U.S. companies.

- All earnings in the account are tax-deferred, and taxes apply only when distributions are made.

- Parents will manage the account until the child turns 18, then the child gains complete control.

- Distributions are not allowed before the child reaches 18. Exceptions for rollovers to ABLE accounts and distributions to beneficiaries are also permitted.

- Distributions are pro-rata, consisting of after-tax contributions (tax-free) and earnings (taxed as ordinary income). Penalties may also apply.

- Distributions in the year the account owner reaches 18 and beyond follow IRA rules. Once distributed, the earnings will be taxed as ordinary income, plus a 10% early withdrawal penalty if the distribution does not meet certain exceptions. Notable exceptions to the penalty include:

- College expenses.

- Home purchase (up to $10,000).

- Disability.

Several tax-deferred investment vehicles are available for parents to save for their children. How do Trump Accounts compare to other options?

Pros:

- Initial $1,000 deposit: This is a nice benefit for newborns and, IF left untouched, would significantly boost retirement savings.

- No earned income requirement: Unlike a Minor’s IRA, which requires the child to have income before they can contribute to the account, Trump Accounts have no earned income rules until age 18.

Being able to save $5,000 per year for retirement 10-15 years before a child would typically begin to earn part-time income could add up IF left untouched until retirement age.

Cons:

- Not necessarily tax advantaged: Trump Accounts don’t offer many tax-saving incentives compared to alternatives.

- 529 plan assets receive tax-free treatment when distributions are used for education, and some states even offer up-front tax deductions or credits for contributions to their state’s plan.

- Assets within UTMA/UGMA brokerage accounts are subject to tax-favored capital gains rates if sold after being held for over a year. All earnings distributed from a Trump Account will be taxed as ordinary income.

- Minor Roth IRAs (if the child has earned income) offer tax-free and penalty-free access to principal contributed to the account, tax-deferred growth, and tax-free distributions in retirement.

Trump account contributions receive no up-front deductions, and a portion of the future distributions will be taxed as ordinary income and possibly have a 10% penalty tacked on top if an exception does not apply.

- Lack of Diversification: Trump accounts can only be invested in funds/ETFs that track the S&P 500 or another index linked primarily to U.S. companies. While U.S. markets have historically provided robust returns, being able to rebalance in and out of uncorrelated asset classes such as international stocks, bonds, and real estate helps generate higher risk-adjusted returns. Access to other asset classes is necessary as a beneficiary gets closer to using the funds for their desired intention (college, home, etc.).

Bottom Line: If you have a new baby or grandchild born before 2029, double congratulations! Ensure you get the Trump Account opened to receive the federal government’s seed money. If you don’t have newborns in your future, there may be better options. Given their restrictions and lack of tax incentives, parents of minors would most likely use Trump Accounts after current tax-advantaged savings options, such as 529 plans and Roth accounts for minors, have been fully utilized, not as a replacement for these accounts. However, everyone’s circumstances are unique, and we would be happy to review your situation with you.

Charitable Giving. Permanent beginning in the 2026 tax year. A charitable deduction was introduced and made permanent for taxpayers who do not itemize their deductions. For taxpayers who itemize their deductions, the OBBB introduced a new floor, or threshold, wherein only itemized charitable contributions in excess of the floor are deductible. Additionally, a tax credit was introduced for contributions given to scholarship-granting organizations.

- Non-Itemizer’s Charitable Deduction

- The deduction is capped at $1,000 for single filers ($2,000/MFJ).

- Contributions must be made in cash to a public charity.

- The taxpayer cannot itemize deductions.

- This deduction is taken after AGI has been calculated and will not lower AGI. It is available to those who claim the standard deduction.

- Itemized charitable contributions

- A new floor of 0.5% of AGI for itemized charitable contributions is introduced.

- All things being equal, the deduction allowed for charitable contributions will be smaller for taxpayers who itemize in the future.

- Planning Opportunity: Bunching charitable contributions and other itemized deductions one year, and taking the standard deduction in alternating years, while still claiming the non-itemizer charitable contribution, may be an opportunity for some taxpayers.

- Tax credit of up to $1,700 for Contributions to Scholarship-Granting Organizations

- The contribution must be in cash.

- The scholarship-granting organization must meet specific criteria and be registered in the state where it grants scholarships.

- Any state tax credit allowed for the same contribution reduces the federal tax credit.

- Contributions taken as a federal tax credit under this provision can not be claimed as deductions elsewhere on the tax return.

Premium Tax Credit. Expiring after 2025. Several changes were made to the Premium Tax Credit. Three changes (one temporary change that was not extended and the other two changes permanently enacted) resulting from the OBBB are the most noteworthy.

First, Congress did not extend the enhanced premium tax credit for higher-income households. Second, the Premium Tax Credit was eliminated for lower-income households in the first tax year of coverage if the household did not meet specific conditions before enrolling. And third, the cap on repayment of the Advanced Premium Tax Credit was removed for all taxpayers.

- The OBBB does not extend the enhanced premium tax credit beyond December 31st, 2025.

- This means individuals with incomes over 400% of the federal poverty level will no longer qualify for any premium tax credit amount and must pay marketplace plan premiums in full.

- To be eligible for the Premium Tax Credit, lower-income households must enroll in Marketplace coverage during the regular enrollment period or due to specific changes in their conditions.

- Lower-income households that enroll outside of these periods as part of a special enrollment period for low-income families (i.e, income less than 150% of the poverty rate) are not eligible for the Premium Tax Credit for that tax year.

- Elimination of the repayment cap of the Advanced Premium Tax Credit.

- Households that received an Advance Premium Tax Credit to offset their monthly insurance premiums, and then later, when they filed their tax return, reported actual income higher than initially estimated, will receive a lower Premium Tax Credit relative to their Advance Premium Tax Credit. All households in this situation must repay the full difference between the Advanced Premium Tax Credit and the Premium Tax Credit as part of their income tax filing.

Other Notable Provisions:

- The Child Tax Credit will increase to $2,200 (up from $2,000) for eligible dependents.

- Beginning in 2026, educator expenses will be allowed as an additional itemized deduction with no limit (formerly $300 cap).

- The Dependent Care FSA contribution limit will increase to $7,500 (up from $5,000).

- Starting in 2026, all Bronze and catastrophic plans available on the health care exchange will be considered qualified HSA plans.

- The federal estate exemption is permanently raised to $15 million per individual and indexed for inflation.

- The OBBB also has many business-related provisions, including full expensing of Research and Development, 100% Bonus Depreciation, and enhanced Opportunity Zone incentives.

The OBBB of 2025 made many permanent and temporary changes to the tax code. In many instances, the changes to the law represented a permanent continuation of the changes made by the Tax Cuts and Jobs Act of 2017. In some other cases, temporary changes were made to the tax code to deliver on campaign promises made during the presidential election cycle. Taken together, there are many new planning opportunities emerging from the changes.

If you would like to discuss how the OBBB impacts your specific tax situation, please reach out and let us know. We would be happy to discuss these changes with you and identify how they may apply to your unique situation. You should also reach out to your tax advisor to discuss these changes.